Introduction

When it comes to insuring luxury or modified vehicles, many car owners assume that paying a higher premium guarantees full protection. However, insurance policies often contain complex valuation methods that can significantly impact the final payout.

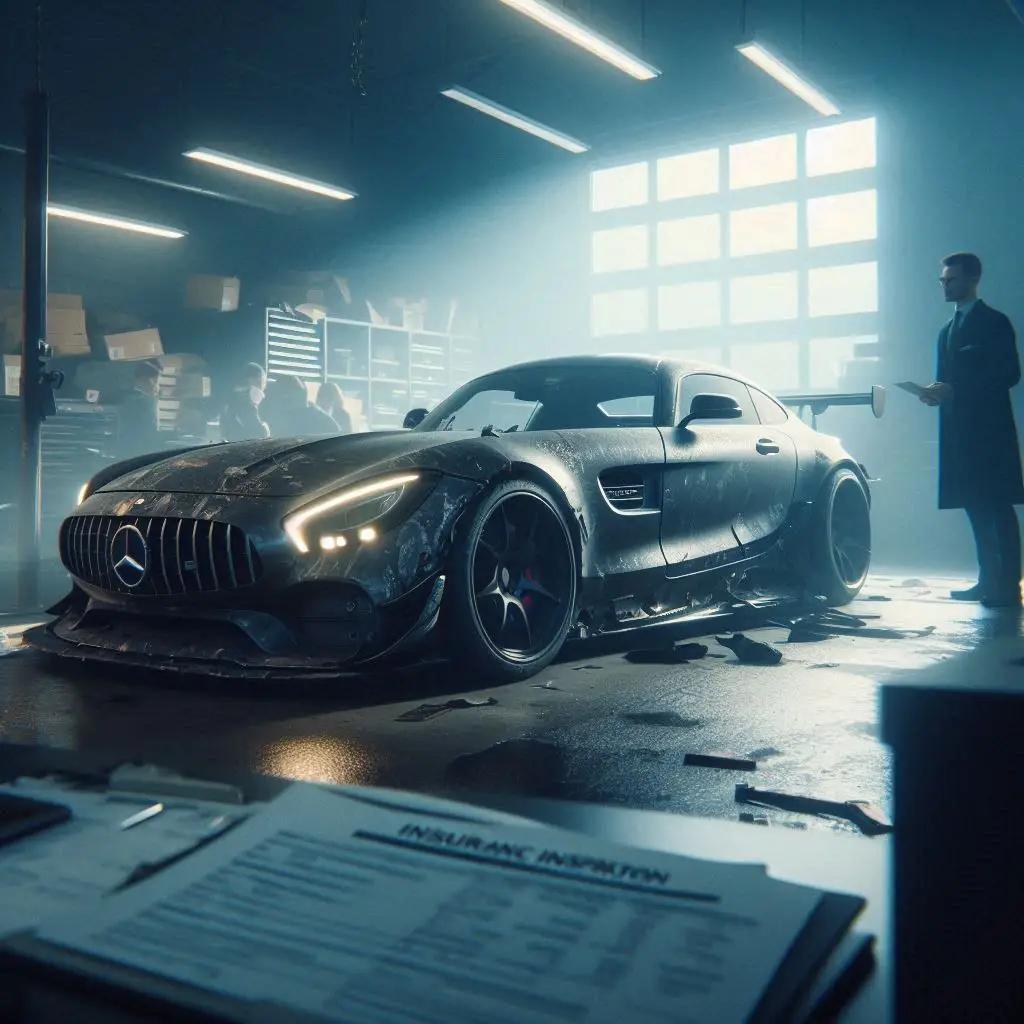

This real-life inspired case highlights a costly misunderstanding between “Stated Value” and “Agreed Value” insurance—one that can lead to losing tens of thousands of dollars after a total loss.

Quick Facts

- Type of Insurance: Auto Insurance (High-Value Vehicle)

- Vehicle: Mercedes AMG GT (Modified)

- Declared Value: $180,000

- Insurance Type: Stated Value Policy

- Main Issue: Lower payout based on Actual Cash Value (ACV)

- Financial Loss: Approximately $50,000

Understanding High-Value Car Insurance

Luxury, exotic, and modified vehicles require specialized insurance coverage due to their unique value. Standard insurance policies often rely on depreciation models that may not reflect the true worth of customized or collector vehicles.

For this reason, insurers offer different valuation methods that determine how much is paid in the event of a total loss.

The Real Story

Mark, a successful businessman, owned a fully customized Mercedes AMG GT. Over time, he invested tens of thousands of dollars in performance upgrades, exhaust systems, and luxury interior enhancements.

These modifications significantly increased the car’s market value, bringing it close to $180,000.

When purchasing his insurance policy, Mark declared this value and paid a higher premium under what he believed would guarantee full compensation if anything happened to his car.

The Shock

After a severe accident, Mark’s vehicle was declared a total loss.

Confident in his coverage, he expected to receive the full $180,000 he had declared.

Instead, the insurance company offered only $130,000.

This unexpected gap left Mark facing a substantial financial loss despite paying high premiums for coverage.

The Insurance Company’s Explanation

The insurer explained that Mark’s policy was based on a “Stated Value” agreement.

Under this type of policy, the insurance company has the right to pay either:

- The stated value declared by the policyholder, or

- The Actual Cash Value (ACV) of the vehicle at the time of the loss

The insurer chose the lower amount, calculating the payout based on the value of a standard Mercedes AMG GT and ignoring the costly modifications.

Legal Insight: Stated Value vs Agreed Value

This case highlights a critical distinction between two key insurance concepts:

Stated Value Policy:

The value declared by the policyholder is primarily used to calculate the premium. However, the insurer can still reassess the car’s market value at the time of the loss and pay the lower amount.

Agreed Value Policy:

A fixed value is agreed upon by both the insurer and the policyholder at the start of the contract. In the event of a total loss, the insurer must pay the full agreed amount without reevaluation.

This difference can have a massive financial impact.

Why This Happens

Insurance companies aim to manage risk and control costs. Stated Value policies give them flexibility, allowing them to adjust payouts based on market conditions.

However, this flexibility often works against the policyholder—especially when the vehicle includes custom upgrades that are difficult to value using standard market comparisons.

Could This Happen to You?

Yes. Many car owners mistakenly believe that declaring a higher value guarantees full coverage.

This misunderstanding is common among owners of:

- Luxury vehicles

- Modified cars

- Collector or classic cars

Without the correct policy type, significant financial losses can occur after an accident.

Common Mistakes to Avoid

| Mistake | Solution |

|---|---|

| Assuming higher premiums guarantee full payout | Understand policy valuation type |

| Choosing Stated Value for modified cars | Opt for Agreed Value policies |

| Not documenting modifications | Keep records and receipts |

| Not reading policy terms | Review contract carefully |

Practical Advice

- Always ask your insurer whether the policy is Stated Value or Agreed Value

- Choose Agreed Value for luxury, exotic, or modified vehicles

- Document all upgrades and keep receipts

- Confirm that the agreed value is clearly written in the policy

- Consider insurers specializing in high-value or collector cars

Awareness Section

Before purchasing insurance for a high-value vehicle, ask specific and direct questions:

- Is this an Agreed Value policy?

- Will the full amount be paid in case of total loss?

- How are modifications valued?

Clear answers to these questions can prevent costly misunderstandings.

FAQ

Q: What is Actual Cash Value (ACV)?

A: It is the depreciated value of the vehicle at the time of the loss.

Q: Is Stated Value the same as guaranteed value?

A: No, it only influences the premium and does not guarantee payout.

Q: Which policy is الأفضل للسيارات الفاخرة؟

A: Agreed Value policy is the best option for high-value vehicles.

Disclaimer

This article is for informational purposes only and does not constitute legal or financial advice.

Conclusion

This case demonstrates how a simple misunderstanding of insurance terminology can lead to major financial loss.

For owners of luxury or modified vehicles, choosing the correct policy type is essential. An Agreed Value policy provides clarity, certainty, and full protection—ensuring that what you insure is truly what you receive.

Sources

- Hagerty – Insurance for collector and exotic cars

- Forbes Advisor – Exotic car insurance insights

- J.D. Power – Auto insurance valuation methods

Author

Written by Carla – Content writer focused on insurance and financial protection topics in the United States.

Website managed by Hicham Asouab, founder of True Insurance Stories.