Introduction

Student loans are often seen as a necessary step toward achieving higher education in the United States. However, behind many of these financial agreements lie hidden risks that can have devastating consequences for families. This real story from New Jersey reveals how a tragic loss turned into a long and painful financial battle due to the fine print of a private student loan agreement.

Understanding how student loan protections work—especially for co-signers—is essential before signing any financial contract.

Quick Facts

- Type: Private Student Loan Death Discharge

- Location: New Jersey, USA

- Main Issue: Co-signer held responsible after borrower’s death

- Loan Amount: Over $50,000

- Outcome: Legal and financial struggle for the family

Understanding Student Loan Protection

Student loans in the United States fall into two main categories: federal loans and private loans. While both help students finance their education, they offer very different levels of protection.

Federal student loans generally include automatic discharge in case of death or permanent disability. This means that the debt is canceled and does not pass on to family members.

Private student loans, however, are issued by banks or commercial lenders. These loans are governed by contracts, and historically, many did not include protections for co-signers in the event of the borrower’s death.

This difference can have serious consequences, as demonstrated in the following real-life case.

The Real Story

In 2001, Christopher Bryski, a young student from New Jersey, had ambitious dreams of completing his university education. Like many families, the cost of tuition was too high to cover without financial assistance.

To help his son pursue his goals, Joseph Bryski agreed to co-sign several private student loans. At the time, this decision seemed like a normal and supportive act of parenthood.

However, tragedy struck when Christopher was involved in a severe accident that left him in a coma. After two years in this condition, he sadly passed away.

While the family was grieving their loss, they were suddenly confronted with an unexpected and devastating reality.

What Happened After the Tragedy?

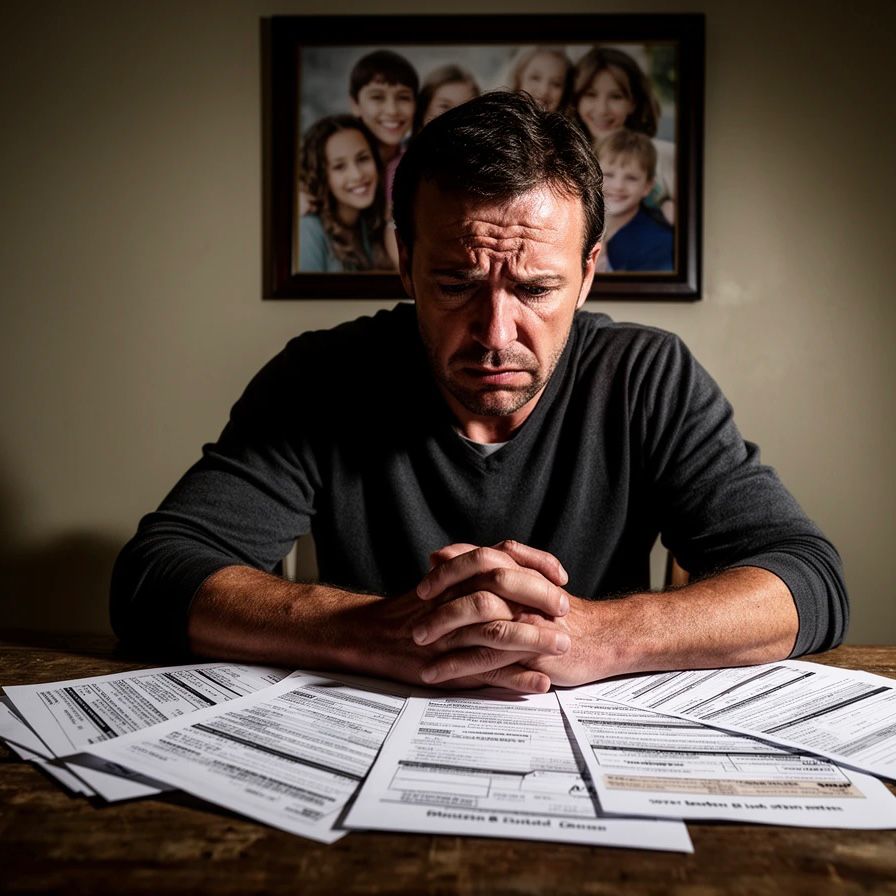

Shortly after Christopher’s death, Joseph Bryski began receiving letters from the lender demanding repayment of more than $50,000 in student loan debt.

Confused and shocked, the family contacted the lender—known at the time as Sallie Mae—hoping the debt would be forgiven due to their son’s death.

Instead, they were informed that the loan agreement did not include a death discharge clause for the co-signer.

This meant that legally, Joseph Bryski was fully responsible for repaying the entire debt.

Legal and Administrative Reality

The lender’s position was based strictly on the loan contract. As a co-signer, Joseph had agreed to repay the loan if the borrower could not.

From a legal standpoint, the lender treated him as equally responsible for the debt.

The situation escalated quickly. The family faced aggressive collection efforts, including:

- Repeated payment demands

- Threats of legal action

- Potential risk to their home and retirement savings

What began as a period of mourning turned into a stressful financial and legal battle.

Legal Insight: Federal vs Private Loans

This case highlights a critical distinction in the U.S. financial system:

- Federal Student Loans: Automatically discharged upon death or permanent disability

- Private Student Loans: Governed by contracts, which may or may not include discharge protections

At the time of this case, many private lenders did not offer death discharge protection for co-signers.

This left families exposed to unexpected financial obligations, even after tragic events.

Impact and Policy Changes

The Bryski case gained national attention and sparked public debate about the fairness of private student loan practices.

As a result, lawmakers introduced the Christopher Bryski Student Loan Protection Act, aimed at increasing transparency and requiring lenders to clearly disclose what happens to loan obligations in the event of death or disability.

While not all issues were resolved immediately, the case played a significant role in raising awareness and encouraging reforms in the industry.

Could This Have Been Avoided?

Partially, yes.

If the loan agreement had included a clear death discharge clause, the co-signer would not have been held responsible.

However, many borrowers and families are not fully aware of these details when signing loan contracts.

Common Mistakes to Avoid

| Mistake | Solution |

|---|---|

| Not reading loan terms carefully | Review all clauses before signing |

| Assuming all loans have protections | Understand differences between federal and private loans |

| Ignoring co-signer responsibility | Recognize full financial liability |

| Relying on verbal assurances | Ensure everything is in writing |

Practical Advice

- Always prioritize federal student loans when possible

- Ask lenders about death and disability discharge policies

- Consider co-signer release options after consistent payments

- Purchase life insurance to cover loan amounts

- Keep copies of all loan agreements

Awareness Section

If you are considering co-signing a student loan, ask this critical question:

“Will the co-signer be released from the loan if the borrower dies or becomes permanently disabled?”

Do not rely on assumptions. Make sure the answer is clearly written in the contract.

Laws and lender policies vary, so taking the time to verify these details can prevent serious financial consequences.

FAQ

Q: Are all student loans canceled after death?

A: No. Federal loans are discharged, but private loans depend on the contract terms.

Q: What is a co-signer?

A: A co-signer is someone who agrees to repay the loan if the borrower cannot.

Q: Can co-signers be released from loans?

A: Some lenders offer co-signer release after a period of on-time payments.

Disclaimer

This article is for informational purposes only and does not constitute legal or financial advice.

Conclusion

This real story from New Jersey shows how a simple financial decision can have long-lasting consequences. While student loans can open doors to education, they can also create serious risks if the terms are not fully understood.

Before signing any loan agreement, especially as a co-signer, it is essential to read the fine print, ask the right questions, and plan for unexpected situations.

Author

Written by Carla, content creator focused on real insurance and financial protection stories in the USA.