The Piano Prodigy’s Silent Betrayal: How a Disability Insurance Claim Collapsed Under Surveillance

The Hands That “Couldn’t Play” — But Could Conquer Mountains

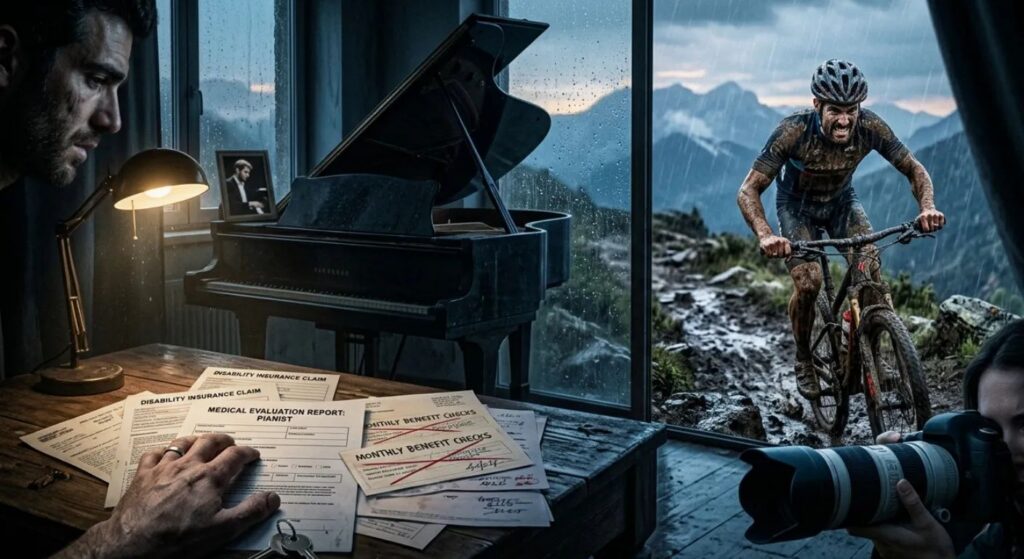

The insurance company believed his hands were permanently destroyed.

According to medical reports, the former piano performer suffered from severe nerve damage that allegedly made it impossible for him to continue his musical career. He claimed his fingers had become too weak and stiff to press piano keys with the precision required for professional performances.

For years, the long-term disability insurance checks arrived every month without interruption.

But while insurers believed he was physically incapable of basic hand coordination, another version of his life was quietly unfolding online.

Public race records and social media photos would eventually reveal a devastating contradiction:

The man who claimed he could barely move his hands was competing in grueling mountain bike races, lifting heavy equipment, and crossing marathon finish lines with both arms raised in victory.

What began as a routine disability insurance claim would soon evolve into a full-scale fraud investigation involving surveillance teams, digital forensic analysis, and behavioral pattern monitoring.

The Anatomy of a Disability Fraud Scheme

From an investigative standpoint, this case represents one of the clearest examples of fraudulent disability claims fueled by what experts call “Lifestyle Contradiction.”

The Original Claim

The musician initially reported that chronic nerve damage and debilitating pain had permanently ended his ability to perform professionally. Medical submissions described reduced dexterity, chronic inflammation, and severe coordination limitations.

Because professional musicians rely heavily on finger precision and repetitive motor control, insurers initially viewed the claim as medically plausible.

The First Red Flags

The case began to unravel during a periodic claim review conducted by the insurer’s Special Investigations Unit (SIU).

Several inconsistencies triggered concern:

- Minimal ongoing treatment: Despite claiming severe impairment, the claimant rarely attended follow-up rehabilitation sessions.

- Physical inconsistencies: Independent medical evaluations showed stronger grip functionality than expected.

- Online activity: Investigators discovered public athletic race registrations connected to his real identity.

The “Impossible Activity” Problem

Insurance medical consultants quickly recognized a major contradiction.

Severe nerve damage capable of ending a professional piano career would normally make high-endurance mountain biking extremely painful — if not impossible.

Long-distance cycling requires:

- Constant grip pressure

- Fine motor control

- Shock absorption through the wrists and fingers

- Rapid hand reflexes on uneven terrain

Yet surveillance footage reportedly showed the claimant navigating rough terrain with remarkable coordination and strength.

How the Insurance Company Exposed the Fraud

The downfall of the claim did not happen inside a doctor’s office.

It happened through digital surveillance, public race databases, and behavioral analytics.

Social Media Surveillance

Investigators uncovered photos and public posts documenting the claimant’s participation in athletic competitions over multiple years.

One image became central to the investigation:

A finish-line photograph showing the claimant gripping mountain bike handlebars firmly while celebrating a race victory.

According to insurance experts, this single image directly contradicted years of medical disability representations.

Field Surveillance Operations

The insurer reportedly hired private investigators specializing in disability insurance surveillance investigations.

Surveillance teams documented:

- Loading heavy sports equipment

- Driving long distances

- Carrying gear with both hands

- Handling athletic equipment without visible discomfort

The evidence package eventually became substantial enough to terminate benefits and initiate financial recovery actions.

Similar large-scale fraud patterns were exposed in other major disability insurance scandals, including the

Long Island Railroad disability fraud scheme

, where investigators uncovered systemic abuse involving corrupt medical evaluations and coordinated false claims.

Cases involving disputed medical limitations have also raised broader concerns about how insurers interpret physical impairment claims, as explored in

The Surgeon’s Shaking Hand disability insurance investigation

, which highlighted the dangerous gray area between legitimate occupational disability and insurer skepticism.

Why Fraudsters Believe They Won’t Get Caught

Academic studies on insurance fraud psychology suggest that many long-term claimants gradually begin rationalizing deception through a process known as Moral Relativism.

Instead of viewing the act as theft, the individual convinces themselves that:

- “The insurance company can afford it.”

- “I paid premiums for years.”

- “I deserve compensation after losing my career.”

Researchers also point to a phenomenon called Identity Collapse.

For professionals whose identity is tied entirely to their career — such as musicians or athletes — losing that identity can create severe emotional instability. Some individuals begin exaggerating symptoms because the financial benefits become psychologically linked to survival and self-worth.

The Rise of AI-Based Insurance Surveillance

Modern disability insurers increasingly use:

- Social media analytics

- Pattern recognition systems

- Public event database monitoring

- Machine-learning fraud scoring

Today, insurers can automatically flag claimants whose online behavior conflicts with their reported physical limitations.

This case became part of a broader industry shift toward data-driven fraud detection systems now widely used in long-term disability insurance investigations.

How Cases Like This Changed Disability Insurance Investigations

Cases involving fraudulent disability claims have dramatically reshaped how insurance companies investigate long-term benefit recipients.

Before the rise of digital surveillance, insurers relied heavily on:

- Medical reports

- Physician statements

- Periodic interviews

Today, insurers increasingly assume that public digital behavior may reveal more than clinical paperwork.

Following multiple high-profile disability fraud scandals — including railroad fraud schemes and public employee disability conspiracies — insurers expanded Special Investigations Units (SIUs) and invested millions into behavioral analytics technology.

Many companies now:

- Monitor public athletic databases

- Review social media metadata

- Cross-reference travel activity

- Analyze geolocation patterns

The industry no longer views disability fraud as isolated deception.

It is now treated as a sophisticated financial crime category.

The Consequences of Disability Insurance Fraud

In the United States, disability insurance fraud can lead to severe civil and criminal penalties.

Once the insurer gathered enough evidence, the claimant reportedly faced:

- Termination of all future disability benefits

- Repayment demands for previously issued funds

- Potential civil fraud litigation

- Major financial penalties

Under U.S. insurance law, knowingly providing false information during a disability claim constitutes Material Misrepresentation.

Even after years of payments, insurers may still:

- Cancel ongoing benefits

- Recover previously paid money

- Refer cases for criminal prosecution

In many states, insurance fraud is prosecuted as a felony offense.

FAQ:

Q: Can disability insurance companies monitor social media?

Yes. Public social media content is commonly reviewed during disability insurance investigations. Photos, athletic activities, travel content, and public videos may all be used as evidence.

Q: What triggers a disability insurance fraud investigation?

Common triggers include inconsistent medical records, suspicious physical activity, anonymous tips, public athletic participation, and lifestyle behavior that contradicts reported disabilities.

Q: Is surveillance legal during a disability claim investigation?

Yes. Insurance investigators may legally observe and record activities occurring in public spaces.

Q: Can disability benefits be canceled after approval?

Absolutely. Approval does not guarantee permanent coverage. Benefits may be terminated if insurers discover evidence of fraud or material misrepresentation.

Q: Can one photo destroy a disability claim?

Yes. A single image showing physical activity inconsistent with medical limitations can become powerful evidence in court or during claim reviews.

The Digital World Never Stops Watching

This case reveals a brutal reality about modern disability insurance investigations:

Your claim no longer lives only inside medical records.

It lives inside:

- Social media platforms

- Race databases

- Public photographs

- Behavioral algorithms

- Surveillance systems

The modern insurance industry operates as a data-driven ecosystem designed to compare what claimants say with how they actually live.

The lesson is simple:

You cannot present yourself as permanently disabled to an insurance company while publicly performing feats that contradict your own medical story.

Sources & References