The Toxic Gala: How DNA Sequencing Exposed Celebrity Chef Business Insurance Fraud

Business insurance fraud has penetrated the high-stakes culinary world, transforming standard kitchen negligence into sophisticated, multi-million dollar corporate liability scams. Imagine an exclusive, black-tie charity gala in Manhattan where 150 elite high-net-worth guests suddenly collapse from severe, life-threatening food poisoning. For Marcus Sterling, an award-winning celebrity chef and restaurant owner, this catastrophic catering event threatened to dissolve his culinary empire overnight. Facing massive impending civil lawsuits from compromised VIP guests, Sterling quickly filed a $600,000 product liability claim, blaming an “unforeseen, contaminated shipment from an external organic farm.” However, a rigorous forensic investigation turned a standard kitchen accident evaluation into a shocking criminal conspiracy of corporate greed and falsified health records.

The Timeline of a Contaminated Kitchen Masterpiece

The operational collapse began forty-eight hours before the grand gala. Chef Marcus Sterling discovered that his primary refrigeration unit had suffered a mechanical breakdown over the weekend, causing thousands of dollars worth of premium raw oysters and imported sea urchins to sit in temperature-compromised environments. Instead of discarding the ruined inventory—which would result in a massive out-of-pocket loss due to an unrenewed equipment breakdown rider—Sterling ordered his kitchen staff to wash the spoiled seafood in chemical sanitizers to mask the odor.

To ensure the event proceeded, Sterling manually forged the kitchen’s daily digital temperature logs and ordered his sous-chef to alter the expiration labels on the seafood crates. The poisoned luxury dishes were subsequently served to the high-profile guests. Within six hours of consumption, over eighty attendees were rushed to emergency rooms across New York City with acute bacterial toxic shock. As public relations panic grew, Sterling proactively initiated a massive commercial insurance claim, completely fabricating a story that the organic supplier had shipped pre-contaminated produce, hoping the insurance company would cover the legal settlements and medical payouts for the victims.

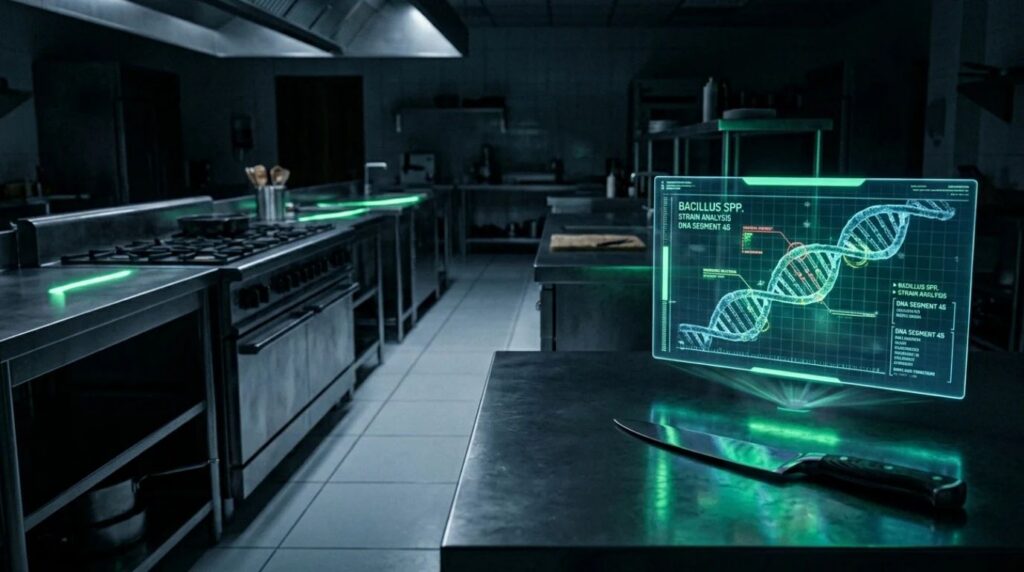

The Anatomy of a Microscopic Culinary Investigation

Why Did the Corporate Deception Happen?

The fraud targeted a severe economic vulnerability within premium hospitality operations: the prioritization of brand prestige over public safety. Sterling’s business was operating on razor-thin profit margins due to aggressive expansion. Admitting to a massive logistical failure and canceling a high-profile gala would cause immediate financial bankruptcy and permanent reputational ruin.

The corporate strategy relied on shifting the total tort liability onto an external, innocent supply chain entity. Sterling assumed that because food poisoning outbreaks are logistically chaotic and involve numerous moving parts, the insurance adjusters would simply settle the legal claims under his general commercial umbrella policy to avoid costly, prolonged litigation.

How Was the Fraud Investigated and Evaluated?

Specialized commercial liability adjusters did not rely on basic kitchen receipts; they deployed forensic epidemiologists and medical investigators to perform a thorough molecular audit. Investigators collected clinical stool samples from the hospitalized victims and cross-referenced them with physical swabbing samples taken from Sterling’s restaurant kitchen drains and cutting boards.

The definitive breakthrough came via **Whole Genome Sequencing (WGS)** of the *Salmonella enterica* bacteria strain. The laboratory data proved a 100% genetic match between the bacteria found inside the restaurant’s faulty refrigeration gaskets and the victims. Furthermore, forensic digital analysts retrieved deleted metadata from the kitchen’s smart logging software, showing that the temperature records were manually updated and overwritten three hours *after* the gala had ended. This pattern of strict technological auditing is uniform across corporate claims; just as forensic teams audit electronic data logs during a trucking insurance fraud case study regarding a phantom cargo heist, hospitality underwriters utilize biological and digital data to uncover deep operational manipulation.

Commercial Liability Claims Adjuster Insight: “In modern hospitality insurance, we no longer debate kitchen staff testimony. Bacteria has its own distinct genetic DNA. When the genetic sequencing matches the internal kitchen environment and contradicts the digital software logs, the corporate fraud case is instantly closed.”

The Hubris Syndrome and Ethical Drift in Premium Industries

To fully understand how a celebrated professional could intentionally poison clients for financial gain, we must examine the academic data on white-collar behavioral drift:

- The Hubris Syndrome in Executive Leadership: Research published in the British Journal of Psychology defines “Hubris Syndrome” as a disorder where highly successful individuals develop an exaggerated pride and contempt for regulatory boundaries, genuinely believing that their professional status exempts them from standard legal enforcement and detection.

- The Concept of Ethical Drift: A business ethics paper from the Harvard Business Review outlines that “ethical drift” occurs when minor, unnoticed deviations in safety protocols are continuously rationalized due to intense corporate stress, eventually leading to a total collapse of core moral frameworks during a major financial crisis.

The Fatal Impact of Intentional Perils

How Does the System Work?

Commercial policies operate under the foundational legal rule of **Fortuity**. Insurance is strictly designed to indemnify businesses against accidental, unexpected events. The moment a corporate entity intentionally alters records, falsifies data, or knowingly deploys hazardous products, the event ceases to be an accident and becomes an intentional criminal act.

Consequently, the carrier invoked the **Fraud and Intentional Acts Exclusion**, canceling Marcus Sterling’s entire commercial liability policy. This left the chef completely exposed to multi-million dollar civil lawsuits from the victims out of his personal pocket. This legal reality mirrors the outcome of any intentional corporate misrepresentation. For example, just as an executive faces total policy termination when falsifying company assets or medical records during a complex workers comp scam investigation involving social media tracking, a business owner who manipulates public health data forfeits all legal protections provided by their commercial insurance contracts.

Key Legal Exclusions in Commercial Liability:

- Product Liability Coverage: Covers accidental food contamination resulting from unintentional processing or supply chain defects.

- Intentional Act Exclusion Clause: Strips away all legal defense and payout obligations if the business owner possessed prior knowledge of the safety hazard and intentionally hid the risk.

Questions (FAQs)

1. Does commercial restaurant insurance cover food poisoning lawsuits?

Yes. General liability and product liability policies cover legal defenses and medical settlements for food poisoning, provided the outbreak was an accidental occurrence and not caused by intentional health code violations.

2. What is Whole Genome Sequencing (WGS) in insurance claims?

It is a highly advanced scientific method that maps the exact genetic DNA of a bacteria strain. Insurance companies use it to trace the precise source of a foodborne illness back to a specific kitchen or supplier.

3. What happens if a business owner falsifies health and safety logs?

Falsifying official safety records constitutes criminal insurance fraud. It immediately invalidates the entire insurance policy, leads to a denial of all active claims, and exposes the owner to heavy fines and imprisonment.

Conclusion

Operating a premium business requires a rigorous adherence to legal regulations, public transparency, and absolute operational ethics. The genetic downfall of Chef Sterling’s toxic gala scam delivers an uncompromised warning to the corporate world: science and digital forensics have made business deception entirely transparent. Attempting to salvage corporate assets by fabricating safety logs is an absolute path to criminal prosecution and financial bankruptcy. Safeguarding your enterprise through legitimate risk management and transparent **business insurance fraud** prevention protocols is the only way to preserve your professional brand and corporate legacy.