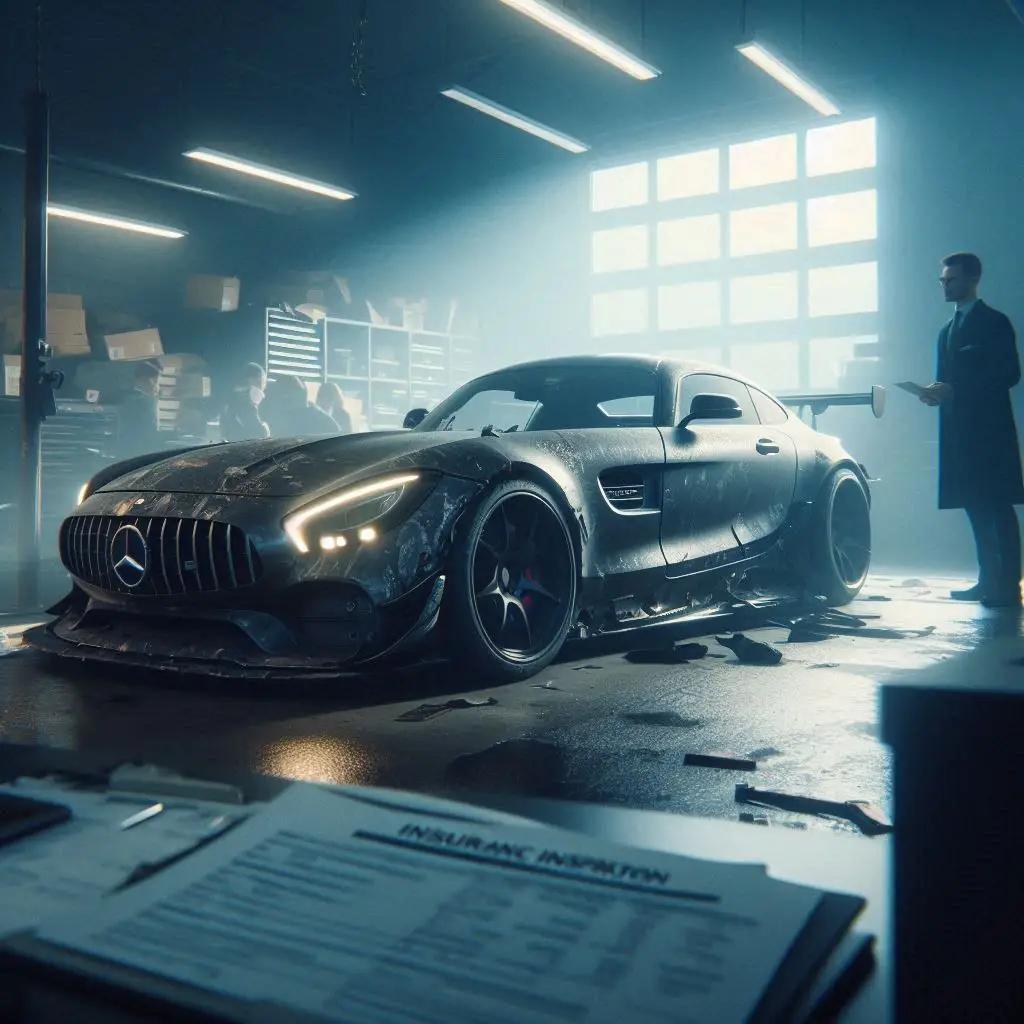

The Counterfeit Ferrari Claim: How Metallurgy Uncovered Exotic Car Insurance Fraud

Exotic car insurance fraud has evolved into a highly sophisticated battleground where elite collectors leverage counterfeit manufacturing against specialized multi-million dollar policies. Imagine the pristine roar of a rare, $1.2 million Ferrari F40 echoing through a private track in Miami, followed instantly by the catastrophic crunch of carbon fiber against a concrete barrier. For Julian Vance, a prominent real estate mogul, the immediate physical destruction of his prize asset was devastating, but the ensuing financial maneuver was entirely calculated. Julian submitted a massive $450,000 property damage claim for the restoration of “100% authentic, numbers-matching vintage components.” However, a meticulous forensic investigation turned a standard accident evaluation into a landmark criminal uncovering that shocked the luxury automotive world.

The Anatomy of a High-End Parts Swap

Why Did the Insurance Fraud Happen?

The fraud targeted a massive financial loophole in the collector market: the exponential valuation contract of matching-numbers heritage parts. Prior to taking the Ferrari to the track, Julian had secretly removed the vehicle’s authentic, factory-stamped transmission and engine casings, storing them safely in a private warehouse. He then retrofitted the vehicle with high-grade, unnumbered aftermarket replicas imported from overseas.

Julian’s objective was to intentionally stage a low-speed track accident, collect the $450,000 payout for “original parts destruction,” use cheap replicas for the repair, and retain the authentic factory components to sell on the black market for an additional fortune. He assumed the adjusters would simply glance at the mangled metal, look at the vehicle’s rare registration, and approve the payout.

How Was the Fraud Investigated and evaluation?

Specialized exotic vehicle adjusters did not just look at the vehicle; they dispatched a team of forensic automotive engineers and metallurgists to conduct a structural audit. Investigators utilized **X-ray fluorescence (XRF) spectrometry** to analyze the elemental composition of the destroyed engine block and suspension arms.

The forensic results were definitive: the aluminum alloy composition lacked the specific chemical signature and trace magnesium ratios utilized by Maranello factories in the early 1990s. Furthermore, under microscopic evaluation, the serial number stampings showed micro-tooling marks indicating they were engraved using modern CNC lasers rather than vintage hydraulic stamps. This deep investigative precision mirrors the strict corporate scrutiny seen in other transport sectors; just as claims teams look for falsified logbooks during a commercial auto insurance truck accident claim investigation, luxury vehicle adjusters look beyond physical paperwork to verify the physical DNA of the asset.

Exotic Asset Claims Director Insight: “In the world of classic and exotic car insurance, we aren’t just insuring a vehicle; we are insuring historical art. If the metal’s DNA doesn’t match the historical record, the contract is completely voided and criminal fraud protocols are triggered immediately.”

The “Value Illusion” and Moral Hazard in High-Net-Worth Markets

To fully understand why affluent individuals engage in high-risk insurance fraud, we must look at the academic and behavioral economic data:

- The Moral Hazard of Agreed Value Contracts: Research published by the Journal of Risk and Insurance explains that “Agreed Value Policies” (common in luxury markets where the payout price is locked regardless of market depreciation) create an artificial economic incentive for artificial claims when the asset’s real-world market liquidity drops.

- The Psychology of White-Collar Risk Rationalization: A criminological study from the Wharton School of Business indicates that high-net-worth fraudsters rarely perceive insurance padding as a traditional theft. Instead, they psychologically view it as an aggressive optimization of paid premiums, believing the insurance company has surplus capital that mitigates the ethical violation.

The Legal and Insurance Lesson: The Severity of Material Misrepresentation

How Does the System Work?

When an exotic vehicle claim involves deliberate manipulation, the carrier invokes the legal doctrine of **Void ab Initio** (void from the beginning) due to fraud and material misrepresentation. This means the entire insurance policy is completely canceled retroactively, and the carrier is legally freed from paying for even the legitimate physical damage sustained during the crash.

Julian was not only left with a completely ruined, uninsurable Ferrari F40, but the case was handed directly to the state’s insurance commissioner for criminal prosecution. This strict legal mechanism is identical across specialized coverage landscapes. Whether a claimant is fabricating automotive metal components or falsifying medical timelines during a highly contested short term disability insurance mental health claim denial appeal, the systemic consequences of misrepresentation remain absolute: total forfeiture of benefits, policy termination, and potential prison time.

Key Legal Differences in Luxury Auto Contracts:

- Stated Value: The carrier pays the Actual Cash Value (depreciated market value) at the time of the accident.

- Agreed Value: The carrier pays a locked, guaranteed amount agreed upon when writing the policy, making it the primary target for intentional staging schemes.

Frequently Asked Questions (FAQs)

1. How do insurance companies verify original parts on rare classic cars?

Carriers hire independent vintage historians, use metallurgic scanning, check historical factory build sheets, and audit the vehicle’s specific continuous chain of custody documentation.

2. What happens if I accidentally use aftermarket parts on an insured classic car?

If done without deceptive intent, it does not constitute fraud, but it can significantly lower your vehicle’s appraised value and payout limits in the event of a total loss claim.

3. Does racetrack driving invalidate my exotic car insurance policy?

Yes. Standard exotic and classic policies strictly exclude any damage sustained while participating in track days, racing events, or timed trials unless a dedicated “Track Day Rider” is purchased separately.

Conclusion

Insuring elite collector vehicles is a highly delicate balance of trust, historical value, and cutting-edge forensic science. The metallurgic collapse of Julian’s Ferrari scheme delivers a powerful warning to the luxury market: technology has made it impossible to deceive modern underwriters. Attempting to exploit a premium contract through structural manipulation is an absolute road to financial and legal ruin. Ensuring your collection is backed by transparent, accurately documented, and legitimate exotic car insurance fraud prevention standards is the only way to preserve both your automotive passion and your personal freedom.