The $2.8 Million Lie That Ended in Death: Inside a Real Life Insurance Fraud Case

The $2.8 Million Lie That Ended in Death

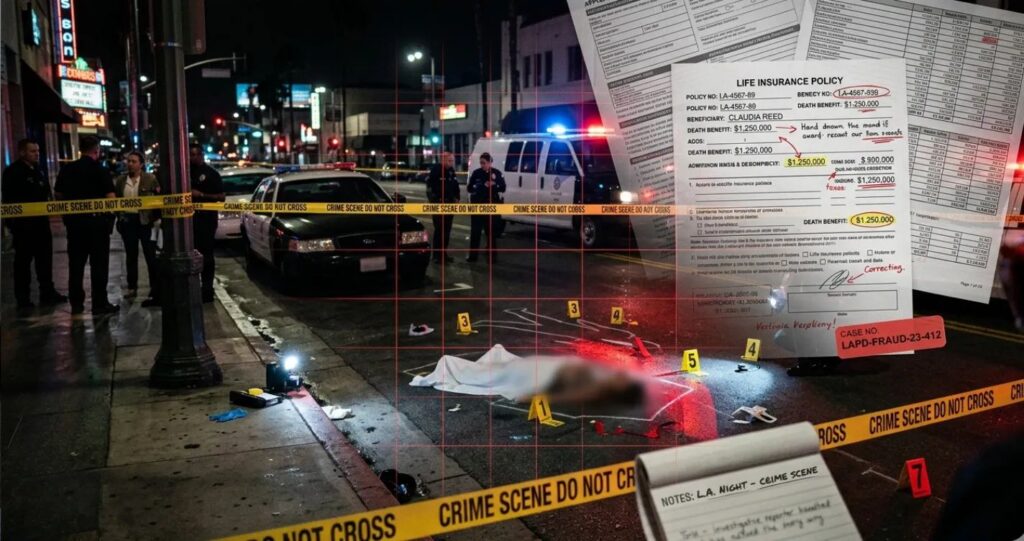

In the streets of Los Angeles, Kenneth McDavid and Kenneth Fitzpatrick were not just homeless men—they became financial assets worth millions on paper.

Behind this transformation were Helen Golay and Olga Rutterschmidt, two women who turned life insurance fraud into a calculated business model.

This was not random crime. It was engineered insurance exploitation.

How the Insurance Trap Was Engineered

How the Victims Were Manipulated

- They presented themselves as helpers

- Provided temporary shelter

- Built emotional trust

- Collected signatures under false pretenses

The victims never realized they had become subjects of insurance policies.

How the Policies Were Purchased

- Creation of financial identities for victims

- False claims of relationships (fiancée, partner)

- Policies issued through major insurers

This exploited a key weakness in insurable interest life insurance.

How the Fraud Passed Insurance Checks

- Weak identity verification systems

- Reliance on paper documentation

- Lack of real-time fraud detection

How the Murders Were Carried Out

- Victims were drugged with sedatives

- Placed in streets at night

- Run over in staged hit-and-run incidents

The deaths appeared accidental—but were intentional.

How Claims Were Filed

- Submission of death certificates

- Insurance claims as listed beneficiaries

- Use of police reports as supporting evidence

This fits directly into life insurance claim investigation frameworks.

How the Money Was Collected

- Hundreds of thousands paid out

- Funds used for personal gain

- Fraud continued undetected for years

How Insurers Detected the Fraud

Pattern Recognition

The case collapsed when insurers noticed repeated patterns:

- Same beneficiary name

- Multiple claims

- Identical cause of death (hit-and-run)

This triggered advanced insurance fraud detection systems.

Data Sharing Systems

Insurers used shared databases like:

ISO ClaimSearch System

Special Investigation Units

- Reopened claims

- Reviewed forensic reports

- Coordinated with law enforcement

Critical Evidence

- Sedatives found in victims’ blood

- No natural behavior before accidents

This shifted the case from accident to criminal insurance fraud.

How This Case Changed the Insurance Industry

Stronger Insurable Interest Rules

- Harder to insure unrelated individuals

- Mandatory proof of financial relationship

Improved Identity Verification

- Integration of financial and legal data

- Reduced identity fraud risk

AI-Based Fraud Detection

- Machine learning pattern analysis

- Real-time anomaly detection

Industry Data Collaboration

- Cross-company fraud databases

- Reduced isolated risk blind spots

Why the Scheme Worked

Incontestability Clause Exploitation

After two years, policies become harder to challenge legally.

The criminals waited deliberately before executing the murders.

System Weakness at the Time

- No behavioral analytics

- No digital verification systems

FAQ

Can you take life insurance on someone else?

Yes, but only if you have a valid insurable interest.

How do insurance companies detect fraud?

- Pattern recognition

- Data sharing systems

- AI fraud detection

What is a life insurance fraud case?

Any attempt to manipulate insurance for financial gain through deception.

How are suspicious claims investigated?

- Medical record review

- Financial pattern analysis

- Law enforcement cooperation

What are common fraud red flags?

- Repeated beneficiaries

- Identical claims

- Unusual financial activity

When Insurance Becomes a Weapon

This case revealed a dangerous truth: insurance systems can be exploited if safeguards fail.

Today, insurance fraud detection is no longer optional—it is essential.

How to Protect Your Finances from Secondary Fraud

While cases like the “Black Widows” are extreme, life insurance fraud can impact regular policyholders through identity theft. To protect your financial protection plans, experts recommend:

- Regular Policy Audits: Check your active policies annually to ensure no unauthorized changes or beneficiaries have been added without your consent.

- Secure Personal Data: Treat your insurance policy numbers with the same level of security as your Social Security number or bank details.

- Verify Agents: Always ensure you are working with licensed professionals by checking the official California Department of Insurance database or your local state regulator.

By staying vigilant, you not only protect your legacy but also help maintain the integrity of the insurance system for everyone.

When Insurance Becomes a Weapon

This case revealed a dangerous truth: insurance systems can be exploited if safeguards fail. The story of the “Black Widows” serves as a stark reminder that life insurance fraud is not a victimless crime—it is a calculated act of predation.

The Key Lesson: In the modern era, insurance fraud detection is no longer optional—it is essential. Data sharing and AI-driven patterns are the new front lines in protecting both the industry and the lives of the vulnerable.

Sources